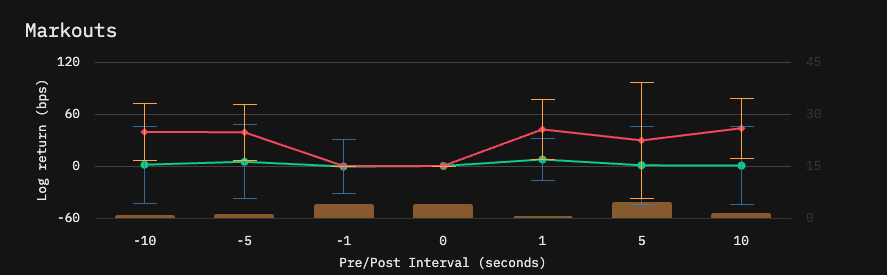

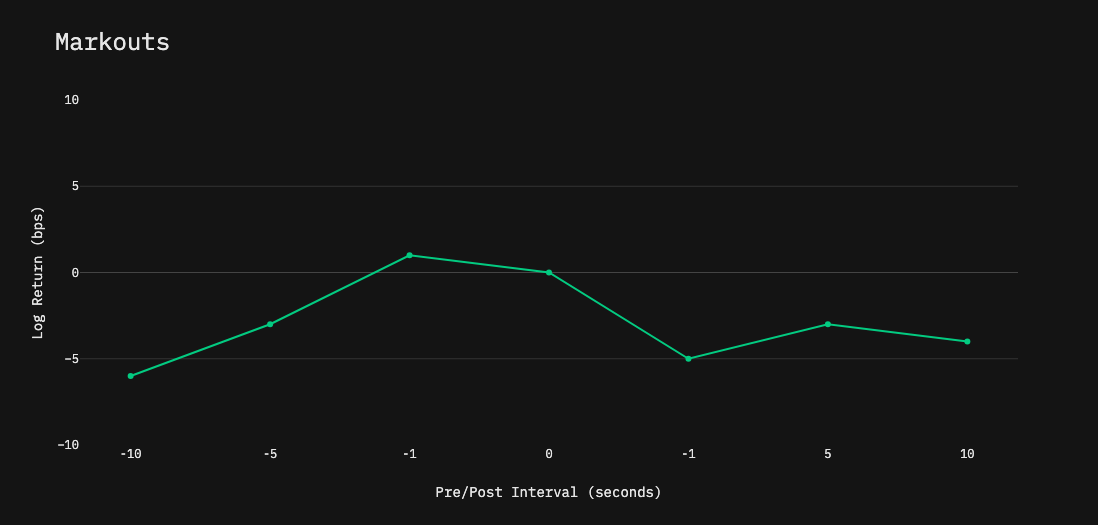

Markouts

Markouts are an aggregation of prices (in log return space) 10, 5 and 1 seconds before and after each individual fill.

Red Line - Taker markouts with error bars (1 SD in orange)

Green Line - Maker markouts with errors bars (1 SD in blue)

Orange Bars - Spread in basis points

The first thing to remember about markouts are that they are defined by sample bias. Maker fills tend to only get filled if the market moves into your resting orders and the engine may rely on taker fills more often when prices are moving away (and resting orders aren't getting filled). Rest assured, as long as you keep this bias in mind, markouts can be immensely helpful in understanding the behavior of other participants on the limit order book and market microstructure that affect your maker/taker rates.

Terminology:

Drift-away - Positive sided returns. If buying, increasing prices and if selling, decreasing prices. Generally a bad thing because prices are getting worse.

Drift-towards. Negative sided returns. If buying, decreasing prices and if selling, increasing prices. Generally a good thing because prices are getting better.

Flat returns: No changes in prices, 0 returns.

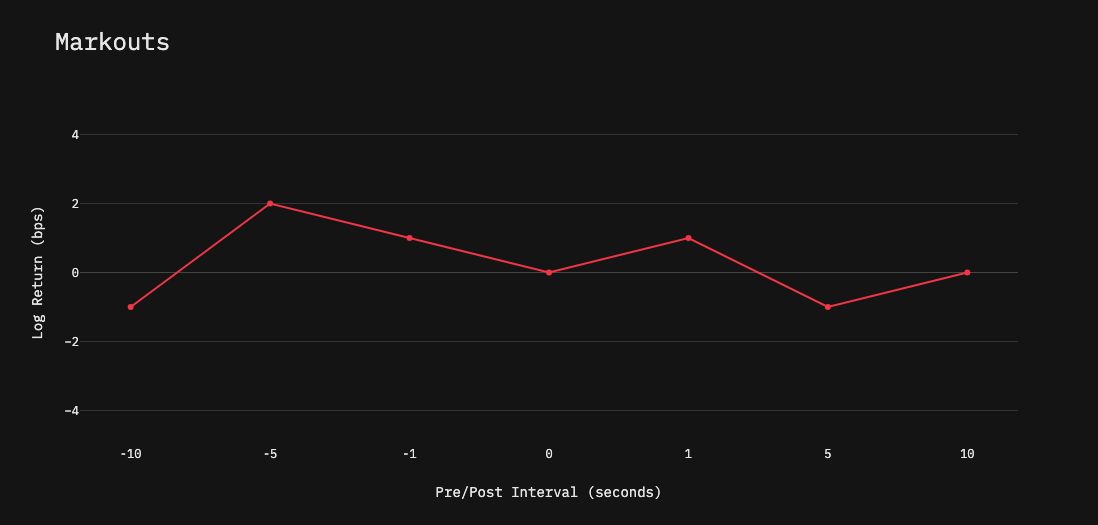

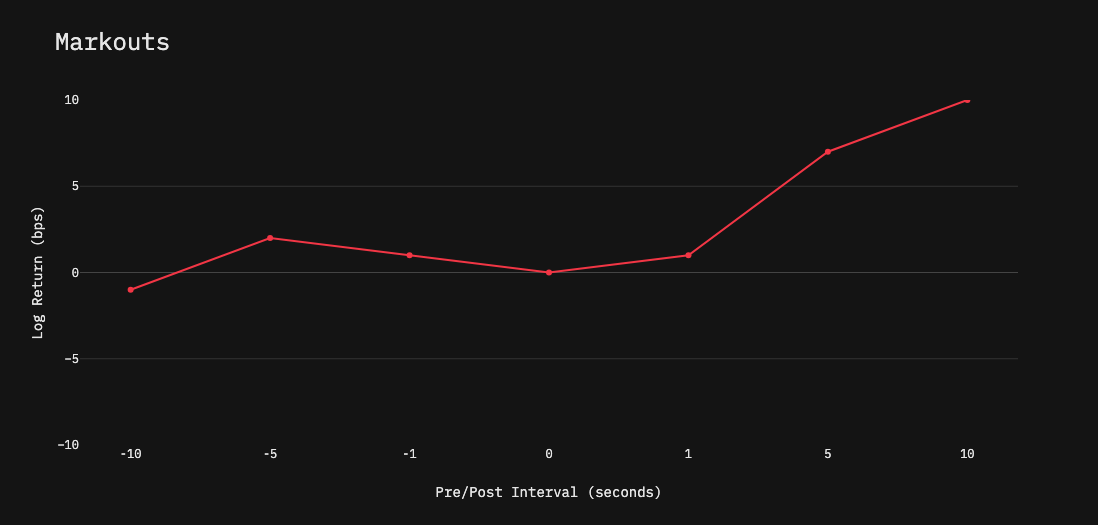

Taker Fills

What you want to see

Minimal impact (flat returns) post-fill. If you see that the price does not move after you get your fill, it is a sign that your aggressive liqudity taking is equaled by resting orders on the other side.

No drift-away pre-fill. If you see the prices moving away before you get your fill, you may be waiting too much on a competitive side to take liquidity. Front-loading your order could coerce the engine to send out more taker orders earlier on the in the order. Note, if your taker fills are very close together, they could be interfering with each other.

What you don't want to see

Drift-away post-fill. If prices move away after the fill, especially 5 and 10 seconds post-fill, your taker orders could be signaling to the makers on the other side about your working order. Once again, if taker fills are coming in very frequently, they may be interfering with each other, so more caution should be given to return profiles that are flat pre-fill and moves away post-fill. If the slope is constant pre/post-fill, there may be external factors at play.

Drift-towards throughout the entire period. You should be getting passive resting orders filled in these drift profiles. You are probably placing too deep in the book and reverting to taking liquidity as a result.

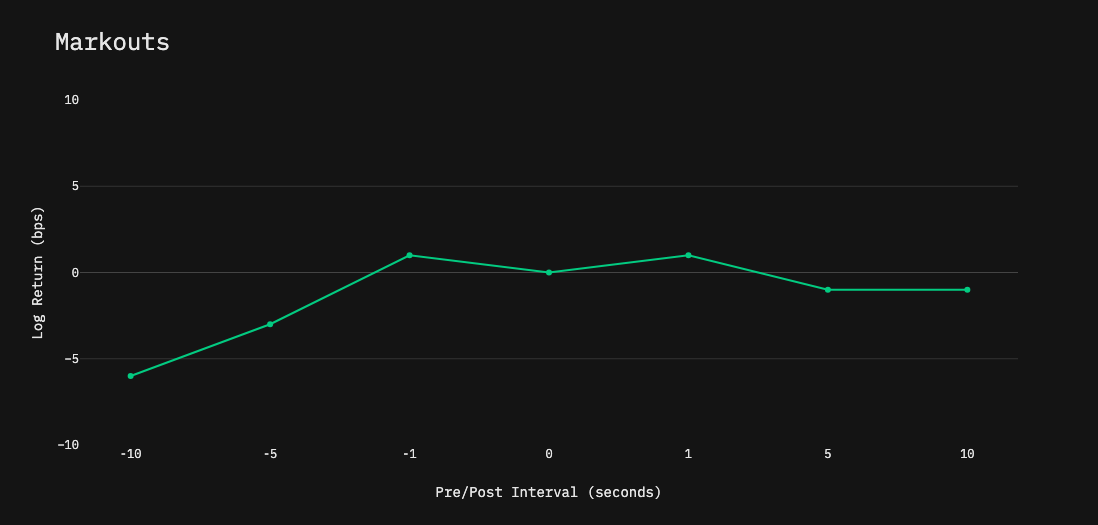

Maker Fills

What you want to see

Drift-towards pre-fill, flat returns post-fill. This is the ideal scenario for when resting orders should get filled. It will almost always be the case as the market has to move towards you for resting orders to get filled, but with the flat returns post-fill, you can be certain that you couldn't have placed deeper in the book and got the resting order filled (adverse selection).

Flat returns throughout. If trading on an illiquid market, this is the best case scenario as you were able to get your resting order filled at near. Had this kind of return profile not resulted in a fill because you were too passive, the engine may have not got the fill at all (if post-only) or had to rely on aggressive taker fills, both scenarios are objectively worse.

What you don't want to see

Drift-towards pre/post-fill. Although the pre-fill returns is normal, seeing drift-towards post-fill indicates that you could have placed deeper in the book and the aggressive parties on the other side would have filled your order (adverse selection).

OTC Fills

What you want to see

Flat. If your OTC trade is making the price move on exchange, your trade may carry too much context to market makers who have influence over prices.

What you don't want to see

Drift-away pre-fill. If you see prices move away from you pre-fill, you are leaking information at the RFQ stage. This is inevitable, but something that should be scrutinized. In crypto, RFQs are generally two sided, so there may be even more suspicious behavior going on by market makers.

Was this helpful?